Opening a bank account is something most of us have done, but have you truly understood the importance of the account name? This critical piece of information links your identity to the account and ensures seamless banking transactions. In this comprehensive guide, we’ll explore everything you need to know about account names for bank accounts – from common examples and naming conventions to verifying and updating your own account name.

What Exactly is an Account Name?

An account name is quite literally the name or names associated with a specific bank account. It’s how the bank identifies the individual(s) or entity that owns and has access to that account. While it may seem straightforward, the account name plays a crucial role in:

- Linking your identity to the account: Your name essentially unlocks and verifies your access and ownership.

- Facilitating transactions: The right name ensures smooth transfers, payments, and account activities.

- Preventing fraud and mixups: Inconsistent or incorrect names can lead to issues accessing your funds.

It’s important to distinguish an account name from the account number. The account number is a unique numerical identifier, while the account name uses the name(s) of the actual owner(s).

Common Examples of Account Names

Account names can look quite different depending on the type of account. Here are some common examples:

Personal Accounts: For individual accounts, the account name will typically be the person’s full first and last name (e.g. John A. Smith).

Joint Accounts: Accounts shared between two or more parties will include multiple names, usually listed one after the other (e.g. Jane D. Doe and Michael R. Sampson).

Business Accounts: Instead of personal names, these accounts use the official name of the business, company, or organization (e.g. Smith & Co. LLC or ABC Charity Foundation Inc.)

Consider this example of how a seemingly clear name discrepancy caused issues:

Marcia had held a savings account under her maiden name “Marcia Caldwell” for years. After getting married and legally changing her name to “Marcia Wilson”, she went to make a withdrawal only to be denied access since the name on the account didn’t match her updated identification. This created unnecessary hassle until the account name could be updated properly.

Components of a Standard Account Name

While naming conventions can vary slightly by bank, there are some typical components that make up a standard personal account name:

First and Last Name For individuals, the bare minimum is the full legal first and last name, with or without middle name/initial.

Middle Name/Initial Some banks may require a middle name or middle initial, while others treat it as optional.

Nicknames Going by a nickname instead of legal first name is generally not accepted (i.e. “Bill” instead of “William”). However, some banks allow nicknames if it’s an official legal name change.

Titles, Suffixes, etc. Professional titles (Dr., Atty.), name suffixes (Jr., Sr., III), and credentials/designations (CPA, PhD) are usually optional add-ons after the core name.

Proper Formatting Consistent name formatting makes account names easier to track. For example:

- Using initials without periods: JA Smith

- Abbreviating suffixes: Jr or III

While seemingly small, these components are important for banks to accurately identify account owners and avoid confusion or naming conflicts.

Recommended This : Does BlueCross BlueShield Insurance Offer Hearing Aid Coverage?

Special Situations for Account Names

Not all accounts are as clear cut as an individual account under one name. Here are some more complex situations that affect account naming:

Joint Accounts For joint accounts with multiple owners, banks typically list out each owner’s full name. The order may or may not matter depending on the bank’s policies.

Example: “John A. Smith and Jane D. Doe”

Name Changes Life events like marriages, divorces, or legal name changes require updating the name on existing accounts to avoid denial of access.

Business Names Businesses can have an official legal name different from the public trade name they operate under. The account name should match the business’ legally registered name.

Custodial Accounts Bank accounts for minors are often opened as custodial accounts under the minor’s name but with an adult as the custodian managing it (e.g. “John D. Smith Jr., minor, Jane A. Smith, custodian”).

Doing Business As” Names Sole proprietors and some partnerships may use a DBA (“Doing Business As”) fictitious name as their account name if properly registered.

Whenever unusual or complex naming situations arise, it’s best to consult directly with the bank about their specific account naming procedures to avoid future issues.

Verifying and Updating Your Account Name

With account names being such a crucial identifier, it’s important to ensure yours is accurate and up-to-date. Inconsistencies between the name on your account and the name on your identification/legal documents could delay or even restrict you from accessing your own funds.

To avoid these problems, here’s how to check and update your account name if needed:

How to Check Your Current Account Name

- Review statements and documents: The account name should be clearly listed on monthly statements, checks, online banking portals, etc.

- Ask a bank representative: If unsure, you can visit a branch or call the bank to inquire what name is officially listed on each of your account(s).

- Use online/mobile banking: Many banks allow you to view and verify your current account name through their digital banking platforms.

Updating an Incorrect or Out-of-Date Account Name

If you find the name associated with your account is wrong or no longer matches your legal/preferred name, you’ll need to update it directly with the bank by:

- Gathering documentation to show your correct, updated legal name (e.g. updated ID, marriage certificate, court order).

- Visiting a branch location or submitting a name change request form online/by mail along with those documents as proof.

- Depending on the bank, you may need to open an entirely new account under the proper name.

After getting married, I brought my marriage certificate to the bank to update my last name from my maiden name ‘Abrams’ to my new legal married name ‘Mitchell,'” recalls Kelly M. “The bank rep made the change across all my accounts in about 10 minutes. So easy!

Why It’s Critical to Update

Keeping your account name updated isn’t just good practice – it’s necessary for conducting smooth banking operations. An old, outdated, or blatantly incorrect name can:

- Prevent you from accessing your own account funds

- Cause issues when providing account details for payments, transfers, direct deposit, etc.

- Lead to tax documentation being improperly issued

- Potentially signal fraud if transactions are made under the wrong name

Bottom line – keeping your account name accurate gives you proper control, access, and peace of mind as the rightful owner. Review your accounts periodically and update as needed to avoid these hassles.

Recommended also This: How to Choose a Solar Installer to Finance B2B

Maintaining Consistent Account Names

Another key aspect of account names? Using the same exact name format consistently across all your banking accounts and institutions.

Most banks have the ability to link accounts together under your name/identity through tools like their Customer Identification Program. However, this linking process works best if you use one standardized version of your name (i.e. “John A. Smith Jr.”) rather than several variations like:

- Account 1: John Smith

- Account 2: J. Smith

- Account 3: John Smith Junr.

- Account 4: Jonathan A. Smith Jr.

While some variations may still link properly, using one consistent name removes guesswork and guarantees your full financial profile can be created. This allows for benefits like:

- Easier account management and oversight across institutions

- Better fraud monitoring and suspicious activity tracking

- Maintaining your full personal identity, credit history, and proof of funds

So once you settle on the preferred name for your accounts (whether personal or business), aim to stick with that exact same naming convention each time you open a new account. Your banking activities will run smoother in the long run.

FAQ

Still have some lingering questions about account names? Here are answers to some frequently asked questions:

Can I use an initial instead of full first name?

Many banks do allow using just an initial for the first name (i.e. J. Smith), though some require the full name to be written out. Always double check their particular requirements when opening a new account.

What if I go by a different name than my legal name?

While you may have a preferred name you go by socially, banks will still require using your full legal name as listed on identification documents for the official account name. This helps prevent fraud. You can update to a new legal name through the courts if you wish.

Do I have to use my middle name?

Including or omitting a middle name is usually flexible as long as you are consistent with the inclusion/exclusion

Here are some additional sections to continue the comprehensive blog post on bank account names:

Make the Most of Online and Mobile Banking

Thanks to modern digital banking, managing your account names and details is easier than ever before. Most major banks now allow you to view and update your account information like:

- Verifying current account names

- Editing/changing account names

- Adding/removing joint account holders

- Opening new accounts with your preferred name

All within the convenience of their online or mobile banking platforms. You can even open a new online account remotely and e-sign disclosures in minutes.

So in addition to making periodic visits to your local branch, take advantage of these self-service digital tools. They provide an easy way to keep your account names organized and up-to-date across all your banking relationships.

Read As This: WHAT ARE THE VIOC CHARGES ON YOUR CREDIT CARD STATEMENT OR BANK STATEMENT?

Business Account Names

To illustrate the importance of proper account naming conventions, let’s take an in-depth look at the nuances of business account names.

Running a business of any size means you’ll likely need to open various accounts – from basic checking and savings to credit accounts, lines of credit, merchant services, and more. Keeping these accounts properly titled and identified is critical.

Here are some common scenarios businesses face:

Legal Name vs. Trade Name Your business likely operates under a public trade name that customers know. However, businesses are registered with the state under their official legal name, which may be worded differently than the trade name.

For example, a plumbing company’s trade name is “John’s Rooter And Plumbing”, but their legally registered name is “John’s Rooter LLC”. The account names should use the legal name as registered to avoid issues.

Multiple Account Holders

Does the business have multiple owners or authorized individuals who need access to the accounts? Their names may need to be included on certain shared accounts.

For example, a partnership business account name may look like: “John A. Smith and Michael B. Jones for Smith & Jones Landscaping Company”.

Changing Business Structure If a business changes its legal structure (e.g. sole prop to LLC), it typically must update registrations and accounts to reflect the new legal name. An account previously under “Joe’s Consulting” may need to be updated to “Joe’s Consulting LLC”.

Branch or Division Account Names Large businesses with multiple branches, subsidiaries or divisions may opt for separate accounts per location/unit with descriptive names identifying each.

For example, “ABC Corp – Arizona Division” and “ABC Corp – Southeastern Regional Office”. This aids in financial reporting and organization.

Authorized Representatives Depending on corporate structure and operating agreements, authorized representatives may need to be named on accounts for transaction and oversight permissions.

For example, “ABC Manufacturing Inc., John A. Smith President, Michael Harper VP of Finance”.

As you can see, there is added complexity when dealing with business accounts compared to personal accounts. Double checking your jurisdiction’s specific requirements and working closely with your bank and/or legal counsel is recommended for setting up proper account names and permissions. Avoiding easily preventable mix-ups is key for ensuring seamless business banking activities.

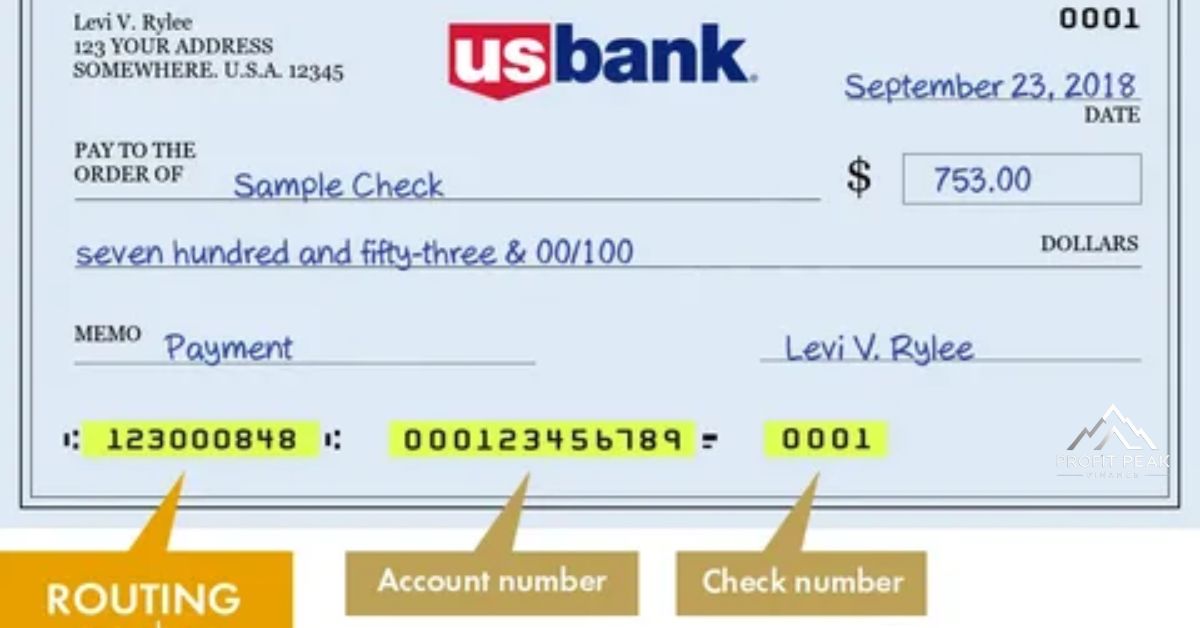

Account Numbers: The Paired Identifier

While the account name is a crucial identifier, it’s always paired with another important piece of information – the account number. Let’s quickly review:

What is an Account Number?

A unique string of numbers and sometimes letters/characters that is assigned to every bank account for identification purposes. This is different than the account name/title using the owner’s name.

Where to Find It

Your account number is listed on statements, checks, online banking accounts – anywhere you see the specific account detailed.

Common Uses Account numbers are used for a multitude of transactions involving that account, including:

- Setting up direct deposits

- Creating payment/billing profiles

- Transferring funds between accounts

- Tax reporting purposes

- Proving account ownership

Account Number Formats Format and length can vary, but common examples are: 12345678912, 8429671-03, 0072900037AS. Numbers are most common but some formats incorporate letters or other characters.

Together with the account name, the account number is an essential identifier that points to a specific bank account. Provide both accurate pieces of information requested to complete transactions smoothly.

Quick Review

To summarize the key points about account names for bank accounts:

- Account names identify the owner(s) of a specific account

- Names should match current legal/official names to avoid access issues

- Conventions vary for personal accounts, joint accounts, businesses, etc.

- Check and update account names after any legal name changes

- Use consistent naming across all your accounts for unified banking

- Account names are always paired with account numbers for full account ID

Far from a trivial detail, your account name is a crucial identifier and access point for your finances. Verify yours is up-to-date and properly listed to conduct banking activities securely and with ease.

The Evolution of Account Names

While account names seem simple today, they’ve actually evolved quite a bit over the history of banking:

Early Account Descriptors

In the earliest days of banking, there were no standardized personal account names. Accounts were often identified by rough descriptors based on location, occupation, holdings, or other notable traits. Some examples could be:

- “Smith the Baker’s Account”

- “Yorkshire Farmer’s Funds”

- “Account for Widow Jones”

The Emergence of Legal Names

As banking became more institutional and record-keeping improved, using legal names registered with authorities became the norm for personal accounts in the 19th century. This avoided confusion and provided a documented way to verify true account ownership.

Accommodating New Name Situations

Over time, the banking system expanded naming conventions to accommodate modern family situations. Joint accounts listed multiple names. Married/maiden names existed on the same account. Kids could have custodial accounts under a parent’s name.

Business Account Standardization While personal account names solidified around legal names, there was a gradual standardizing process for business accounts as incorporation rules developed. This allowed official registered business names to become the required naming convention instead of informal names or owner names.

Numerical Identifiers Assigned As the number of open accounts multiplied, banks could no longer rely on names alone to uniquely identify accounts. This led to the introductions of account numbers – numerical identifiers assigned to each account to differentiate and organize them.

Impact of Digital/Online Banking Then in recent decades, the rise of online banking brought even more stringent account naming requirements. Since customers could access their own information remotely, following strict naming conventions and being able to efficiently identify accounts by name became critical.

So while it may feel fundamental today, the modern concept of an account name was an evolving practice shaped by the needs of an increasingly complex banking system over centuries.

Here are some additional sections to further expand the comprehensive blog post on bank account names:

Read Also As This :Can You Get A Mortgage On A House With Foundation Problems In Florida

Funny Historical Names and Mixups

Given the cruder, non-standardized naming practices of early banking, there are some amusing historical examples of unusual and mistaken account names:

In 1734, there is a record of someone opening an account at Ackermann Bank in Germany under the unique name “The Clogmaker With No Toes”. Who knows what unfortunate situation inspired that name descriptor!

Sometimes names caused actual ownership confusion that had to be resolved:

An 1826 court filing shows legal action between the Bank of Maryland and a female customer named Sarah Richards. The bank had mistakenly opened two separate accounts for “Miss Sarah Richards the Seamstress” and “Mrs. Sarah Richards the Baker” thinking they were different people, when they were one and the same!

Even esteemed historical figures got in on the fun names:

When opening his first bank account as a young man, we know Andrew Jackson briefly went by the unique account name “Noliche Hunitse” or “One Who Walks Tall”. It was supposedly a Cherokee name meaning “One Who Walks Tall At Full Gait”.

With no formalized system, it led to plenty of amusing anecdotes. While strange by today’s standards, these names illustrate the more personal, informal relationship between customers and their friendly local bank in centuries past. As always, though, too much irregularity invites error and confusion – necessitating today’s standardized conventions.

International Perspectives on Account Names

Account naming standards can vary around the world based on cultural norms and regional banking regulations. Let’s look at a few examples:

Asia In parts of Asia like China and Korea, accounts traditionally used the family surname first followed by the personal name, reflecting different naming customs. So “Zhang San” instead of “San Zhang”. Some banks still maintain these surname-first account name options.

Middle East

In many Arabic nations, accounts incorporate elements like family/clan names, father’s names, grandfathers’ names and other genealogical identifiers. An account name could appear as “Kareem ibn Ahmed ibn Khalil Al-Rahman”.

Hispanic Naming Hispanics often have two surnames – the paternal and maternal family names. So an account name may need to reflect both surnames together (Jose Antonio Ramirez Espinosa) versus just one.

Professional Titles In places with very structured class/hierarchical systems, including professional titles, honorifics, and other status nomenclature in account names may be expected. For example, “Dr. Vihaan Singhania, IAS Commissioner”.

While built on similar core principles, these cultural details illustrate how account naming is far from universal practice across the globe. International banks and those operating in multiple regions need robust systems to accommodate these diverse preferences.

How To Check If Your Account Name is Consistent

Given the importance of consistent account naming we discussed, here’s a quick checklist you can use to audit your various accounts:

Make a list of all your personal banking accounts across different institutions

For each account, verify and record the full exact name listed [] Check for any differences in how your name appears (i.e. middle name, middle initial, suffix like Jr., etc.) Note any still active accounts that may have old names from before any legal name changes. Do the same for any business accounts, looking at how different banks display the full legal name

Once compiled, you’ll be able to identify any inconsistencies and prioritize important accounts to update if needed. Standardizing one “official” name convention to use for all future accounts can then minimize headaches down the road.

For the super organized, you can even take things a step further:

Create separate lists for personal accounts vs. business accounts if you have both [] Add columns noting each account’s purpose (savings, checking, credit card, etc.) [] Include specific details like account numbers, open dates, and maturity dates

Keeping this master account name log updated annually can help you stay on top of all your banking relationships and account identities. It only takes a little maintenance to save you from bigger headaches of accounts becoming misaligned or inaccessible due to names.

Names and Account Security

Your account name plays a pivotal role not just for identification, but also banking security and fraud prevention. Here’s how:

Name Matching Protocols Most banks have stringent security protocols around confirming the name on an account matches the identity of whoever is trying to access that account. This could involve:

- Showing valid, non-expired government ID with a matching name

- Answering personal security questions about name, address history, etc.

- Having the name match internal bank records based on original account opening documentation

If there are any discrepancies between the account name and the identity presented, it raises a red flag. Transactions may be blocked until identity can be properly verified.

Fraud/Theft Deterrence These name matching requirements exist to thwart fraudsters or thieves from gaining unauthorized access to accounts they don’t own. It prevents scenarios like:

- Using a fake or stolen identity to siphon funds from someone else’s account

- An estranged spouse trying to improperly access a joint account

- Elaborate scams building fake profiles under other identities

Monitoring for Suspicious Activity

Beyond just initial access, banks utilize account names to monitor for patterns of suspicious transactional behavior. If they notice transactions being frequently conducted under various name aliases or unconnected identities on a single account, it could trigger an investigation into potential fraudulent activity.

Enhanced Digital Security With more customers banking online and across devices, having an account name that is definitively tied to your profile and identity becomes even more crucial for security. It prevents unauthorized remote access and preserves privacy.

So in many ways, keeping your account name information accurate is as much about security as it is about simple identification and organization. Don’t underestimate this in helping safeguard your money and financial activities.

Account Name Red Flags

On the flip side, there are certain account name “red flags” that banking institutions are trained to be wary of. While not necessarily indicative of actual fraud, these may prompt additional scrutiny:

Unusual Name Formats or Characters Account names with odd characters, numbers, or strings of special symbols/emojis intermixed could be signs of fraudulent name obfuscation.

Creative Misspellings or Look-Alike Names Names that appear to be attempting clever misspellings of common names (e.g. “Jhon Smyth”) are suspect.

Excessive Name Length Extremely long account names stretching beyond normal name lengths raise questions about their legitimacy.

Lack of Clear Name Pattern For businesses, accounts listing generic terms or descriptions instead of clearly formatted legal names are suspect (“Payment Holding Account 123”).

Multiple Name Variations If a customer or business has a high number of accounts with many differing name formats, it sets off anti-money laundering flags.

Negative News Bank monitoring systems are trained to be cautious of account names associated with negative news, sanctions, illegal activities, etc.

While not inherently bad, these types of outlier account names tend to receive extra scrutiny and verification steps from banks to validate nothing nefarious is occurring. It underscores the importance of sticking to normal, clearly established name conventions in your banking activities.